For those not involved in the financial industry, it is a minefield, covering multiple facets and for a layman like me, it’s somewhat confusing as to what type of finance help I might need to help get the most out of my life. For example, I’m not sure of the differences between a Financial Adviser and a Financial Planner which means I don’t know which I should talk to and for what type of advice? With that in mind, I had a long chat with Alan to really get to grips with what the titles actually mean. The fog has cleared – I know what a Financial Planner is and I can tell you something, everyone should have one (there’s really no need for a Financial Adviser when you have a Financial Planner).

The Human Approach

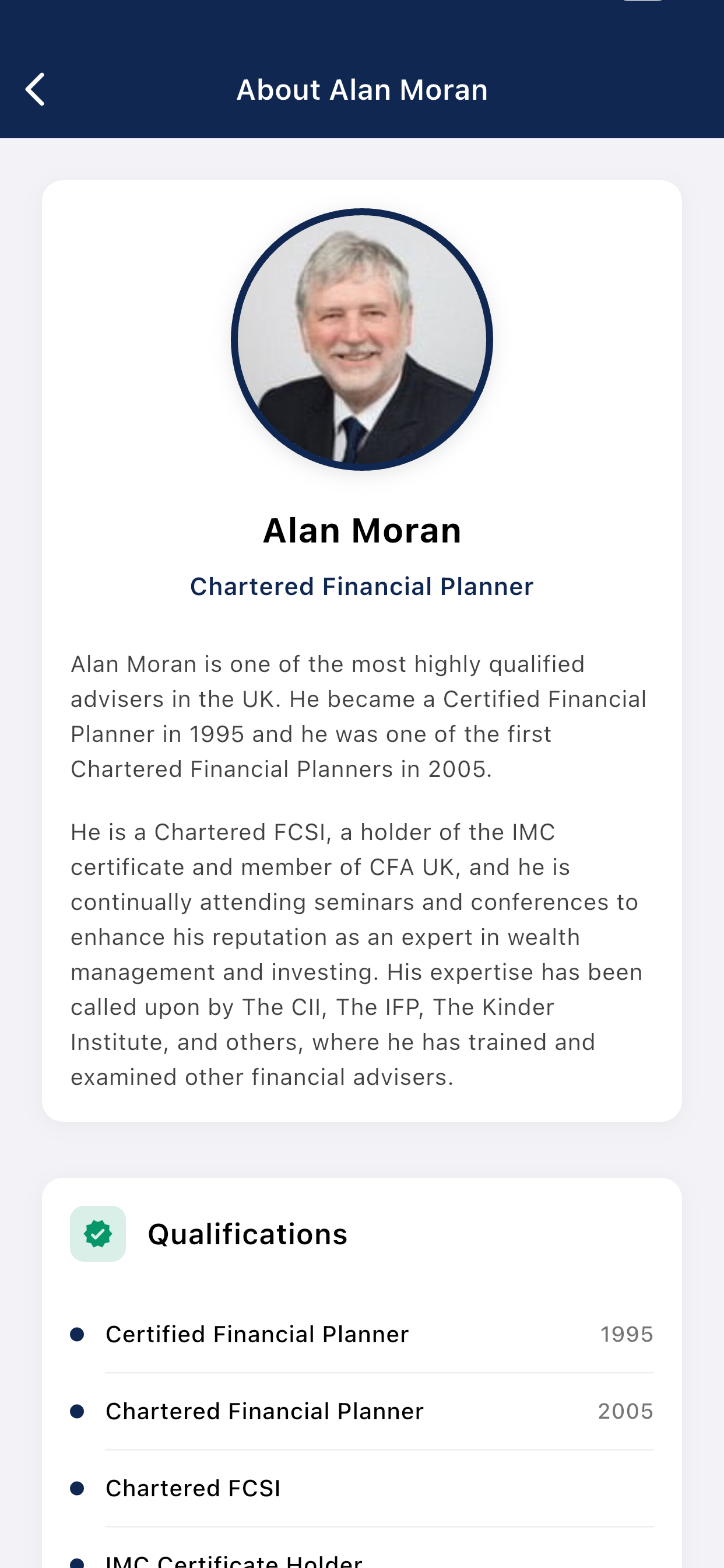

Alan is a Certified Financial Planner (more about this later), and his financial planning involves a genuinely human approach. Listening to Alan, I think that’s the essence of financial planning. It is client-centred and is very much about life planning.

Alan is all about the people he talks to, his clients. The finance side, while obviously important, is secondary. I’ll explain more in a moment but one of the things that Alan really stressed to me is that he wants to make a difference to people’s lives. He’s not about lining his pockets – as so many Financial Advisers are. Financial Advisers let money rule their life whereas Financial Planners use it as a tool to enhance their clients’ lives where necessary and if necessary. Often, Alan gets approached by new clients that have already been to a Financial Adviser and it greatly upsets him when he hears what they’ve advised, especially when it doesn’t fit in with what the client wants to achieve.

Chartered Financial Planner V Certified Financial Planner

Next, let’s look at the title Financial Planner. The Chartered Insurance Institute use name “planner” referring to their advisers as Chartered Financial Planners but the truth is, the majority of those “planners” don’t plan at all, they just advise. Alan is a Certified Financial Planner. The difference is to actually obtain that title; he needs to conduct an annual assessment. That’s not required for the Chartered Insurance Institute and they give out the title without any thought at all. That’s why real Financial Planners find it difficult to describe what they do.

There was a personal finance society a few years ago that conducted a study and concluded that it took an average of 90 seconds into a client meeting with a Financial Adviser before the adviser mentioned pensions and investments. Ninety seconds! What does that tell you? You wouldn’t let someone tell you that you should buy a house in an area you’d never visited at a price that you didn’t think you could afford without really taking the time to do your research and knowing exactly what you wanted out of a home would you? Or book a holiday to somewhere you don’t want to go at a time that’s inconvenient to you and that you can’t afford, involving flying – when you hate flying? That’s exactly what Financial Advisers do. They sell a product without taking the time (and it does take time) to get to know the client, doing some planning and finding out what they want out of life.

Financial Planners Delve Deep

A Financial Planner might talk to their client for hours over several weeks before even mentioning pensions or investments (unless of course it’s absolutely urgent). This is because they want to get to know their client and what makes them tick. What they want to achieve over their life? What their goals are? What their bucket list is (have a look at the bucket list blog here)? They might look at where a pension would fit. A really good Financial Planner (like Alan) will look at even more; family longevity, client lifestyle and client health for example, because all of these factors change priorities. A client might decide after several conversations they’re not ready for a pension or that they’ve decided that the conversations have inspired them to take a few years out to travel round the world before they settle down and think about their future and their finances. The bottom line is, a Financial Planner delves deep to find out what his or her clients really want out of life – and only then do they look at where their finances slot in.

Alan’s Hats

So, back to Alan. He told me that he wear three rather fabulous hats!

Hat One

He gets to grips with understanding his clients’ lifestyles, what they want, what their values are and what makes them tick.

Hat Two

He’s a number cruncher but that’s after he gets to know his clients and then he looks at all aspects of finance; that means income, expenditure, lifestyle projections and more. This is to determine whether his client has enough to live the life he or she wants or if they’re going to run out of money! Next it’s…

Hat Three

This is when the advice comes into play. Alan’s role is to make sure his clients have enough money to do all the things they want to do! It’s at this point he looks at risk. Where are his clients wasting money? He looks at expenditure in detail, queries the stuff that’s just not necessary. For example, the gym membership month after month (when someone hasn’t stepped foot inside the gym for yonks!), that monthly subscription to a number of magazines, never looked at! Those Starbucks coffees three times a day – oh and obviously bigger things too, the 4 x 4 car that runs on diesel but the kids have grown up, is that car necessary? This is all known as “squandered” money. Alan’s job is to get his clients in control of their money first. Then he can look at their lifetime cash-flow and then he can help them PLAN. That planning is important to make sure his clients achieve what they want out of life.

Alan’s hats are nothing to do with pensions and investments! Once his clients are happy with their PLAN it’s only then that he moves onto financial advice.

On a final note, Alan gave me a great example of how brilliantly his financial planning works. About 20 years ago, a lady came to him seeking help. She was in debt, with no money, her lifetime financial projection was concerning, she simply didn’t have enough to retire on (although that was years away at the time). Alan helped her and they’re still in contact today. She recently left him a testimonial and said that now she’s coming up for retirement, she’s happily married and really content with her finances – 20 years of planning means she can retire comfortably and enjoy life. Alan told me that stories like this makes him feel great – he didn’t earn much from her, but she’s happy and that makes him happy too.

It’s no surprise then, that Alan’s business is listed in The Times every year and will be again this coming January, complete with uplifting referrals. Financial planning can change lives. Alan can change your life.